Don’t worry, be happy? Worry a little, but let the data and facts guide and calm

Read time: 13 minutes

Less than a month to go before “halftime” in 2026 and, so far, global equity returns are solidly good. The S&P 500 has advanced almost 11% in price through May, while the small cap laden Russell 2000 index has surged almost 18% in price.

On the international front, EAFE, the well-known developed country international equity index, has kept pace with the S&P 500’s almost double-digit price return through the first five months of the year, returning 7%. Impressively, emerging market stocks that comprise the EEM have bested all the other major equity indices, climbing 23% on a year-to-date basis! Who would’ve guessed in a year of such dramatic news flow?1

Interestingly, we’ve heard from more than a few investment strategists who regularly interact with the media that they sure would have been much more stingy/bearish about their economic and equity return forecast for 2026 had they known in advance that this war was going to happen in the early innings of 2026.

While that might reflexively make some sense, we’ve felt quite differently. This is due to our disciplined process and laser focus on monitoring the actual trends in fundamental, valuation and technical metrics (the FVTs) which have remained supportive of further market advancement throughout.

While the human costs of war and associated suffering are horrible, from an investment and economic standpoint we don’t prophesize or speculate about what MAY happen and what the impacts MIGHT be.

We stick to monitoring the earnings and economic data being released and reported—in other words, the facts. Only when they change do we change our view. We think this has made all the difference. If war is going to be an issue for the market, that will be captured in the trends in earnings, profit margins, employment levels, economic growth, interest rates and credit spreads. On these fronts: so far, so good.

Our constructive message to expect a fourth consecutive year of double-digit stock returns this year, and our associated advice to stay balanced and reduce concentrations, in-the-midst of war-related bearish headlines, lie at the heart of our 2026 Risk Awareness and Diversification 2.0 (RAD) investment thesis that we outlined in our Crystal Ball Market Outlook back in January. The positive results across the various domestic and international equity indices highlighted above, as well the broadening number of stocks and sectors contributing to positive results within the S&P 500 this year, affirm our RAD expectations and advice to be balanced in portfolio positioning.

It’s not just technology or just large cap U.S. stocks that are doing well. Performance is broad based and we think client positioning should be also to do well. Yes, it’s true that after stock market leadership broadened out significantly from October 2025 through February 2026 to include stocks in a number of different sectors than just technology, S&P Tech did resume its leadership status and regain its outperformance edge again in the March to May period after the war broke out.

That said, it’s important to note that it’s not the big Mega 8 names that have led over these last several months; it’s instead been primarily those previously less hyped names in tech, largely in memory, cybersecurity, semi-equipment and semis that have ripped; we’re talking 40% to 200%+ in just a couple of months based on robust revenue and earnings growth, not on aspirations and hopes and dreams.

For example, Mega 8 constituents such as Nvidia and Microsoft are flat and Meta is down over the last month, while Micron, Qualcomm, and Advanced Micro are up more than 85%, 60%, and 50% respectively.1 That’s a wow! Being diversified has been important.

Further, our positive, yet measured messaging has hopefully helped our clients avoid spring whiplash! Again! In the early goings of both 2025 and 2026, our relentless focus on the still solid trends in the FVTs helped us stay objective and avoid becoming prematurely bearish at moments of doubt and vicious swings in investor mood.

Just like in spring of 2025, spring 2026 has delivered a stunningly positive reversal in stock market fortunes on the heels of an Iranian war-inspired February/March swoon. Specifically, the S&P 500 has surged back to new all-time highs following an almost 10% intra-year correction in that two-month period of Feb/March and a drama laden 5%+ decline in the month of March alone when the bombing in Iran and surrounding countries was at its most violent level.

However, since then, the market has rallied more than 19% off the March 27 low through the end of May. On the wings of news that U.S. consumers are still spending in healthy fashion on both services and gadgets, the U.S. labor market is stabilizing, capital spending is amazingly robust in this new world of artificial intelligence (AI), and earnings and profit margins are soaring.1 At a price level of roughly 7,580 as of the end of May, the S&P 500 looks well on its way to our base case of 7,700 and optimistic scenario of 8,100 by year end.

Last year, investors saw a similar roller coaster-like shift. After a sharp sell-off from February through early April 2025 that approached 20%, stocks staged a mid- to late-April renaissance. That rebound ultimately turned into an almost 40% rocket ship ride for the S&P 500 over the final eight months of 2025.

The culprit was shocking “liberation day” tariff rhetoric from the White House Administration. Thankfully, that rhetoric calmed and ultimately dissipated in rather stealth fashion through a “TTO,” or tariff timeout.

The antagonist this spring that caused the temporary disruption in stock prices centers squarely on fears of the potential consequences of war and associated impacts of rising oil prices and the closing of the Strait of Hormuz, rather than the tariff policy woes of last year. The point though, is that in both spring periods, the equity markets justifiably demonstrated an uncanny ability to climb that wall of worry, based on the resilient FVTs.

The April/May rebounds in both 2025 and 2026, driven by strong fundamentals and improved valuation, are just two of many reminders that reducing equity allocations prematurely based headline fears can be costly, especially when those fears haven’t yet meaningfully affected the economic and earnings backdrop.

To clarify, we are not in “all-clear” mode regarding Iran, and we fully expect other evolving risks to continue creating volatility as the year progresses. That said, we’ll take our queue from the trend in the FVTs, which remains positive, not from speculation and prophecy contained in media headlines. Hence, we continue to look for healthy stock returns and urge diversified positioning in equities this year from a sector, geographic, style, and market cap basis.

The Fs—fundamentals—look solid…certainly better than feared!

- Economic data—still in expansion and mostly positive trend: While inflation creep is getting significant headlines, most all other releases of economic data have been positive the last several months. Payroll growth was far better than expected in March with gains of 185,000 new jobs reported for the month, causing the unemployment rate to fall back down to 4.3%—very healthy and low historically.2

Coupled with low unemployment claims and rising job openings, this suggests labor market conditions are solid. This is driving consumer spending and solid retail sales growth. AI-driven capital spending is expected to be over $200 billion higher in 2026 than 2025, higher than expected, and is being revised up for 2027—this is a serious boost to GDP growth.3

Even manufacturing has turned into a bright spot, with the ISM manufacturing PMI Index above the critical 50 threshold for a fifth consecutive month, signaling continued expansion after several years of depressed sentiment. The Atlanta Fed’s forecast for Q2 GDP growth shows our economy pacing at over 4% real growth this quarter.

Financial conditions remain supportive as well. Credit spreads widened modestly during the height of the Iran-related uncertainty, but they quickly snapped back in April and remain tight by historical standards. Put it all together—resilient spending, improving industrial activity and still-benign credit conditions—and the fundamental picture remains firm.

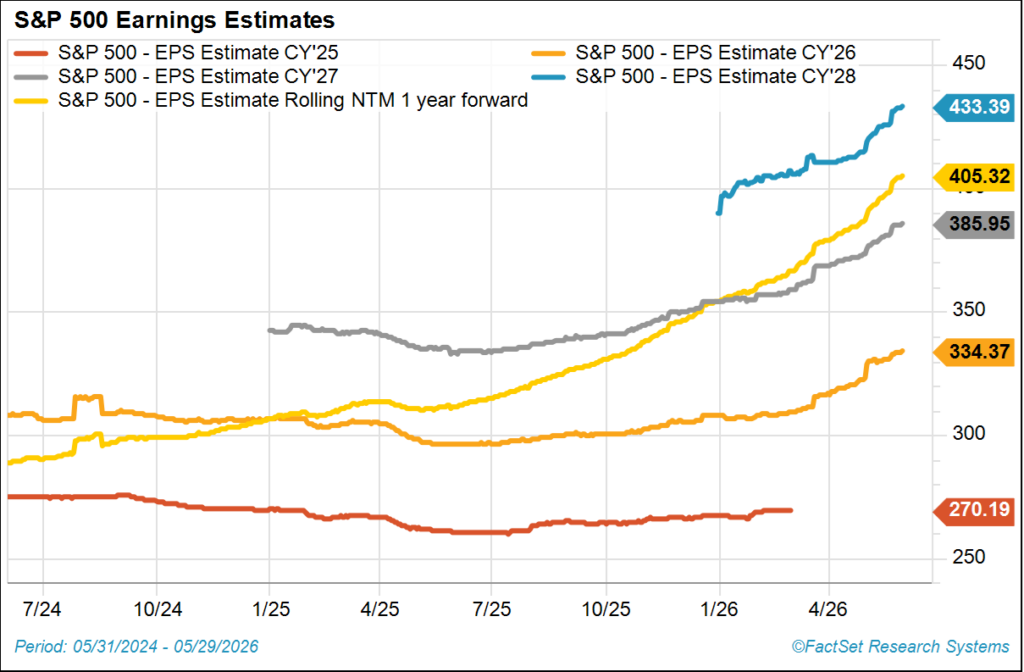

- Earnings are stellar. To employ a play or twist on a famous 1990’s Presidential debate quote, “It’s the earnings, stupid”: They’re simply shockingly good and it’s hard to get bearish when earnings are this robust and broadly positive. S&P EPS growth of more than 25% for Q1 has come in twice as strong as expected; calendar year 2026 earnings growth has been revised up from 15% to 20%.4

Earnings breadth is widening, with 85% of companies reporting upward revisions to earnings in Q1. Earnings are of high quality, with 89% of companies reporting positive revisions in revenue expectations that were already robust. Impressively, all the gains this year in the S&P 500 index have come from earnings growth, not multiple expansion. The S&P 500 P/E multiple has actually contracted this year in the midst of this strong earnings growth.

Finally, we find it noteworthy that 2027 S&P 500 consensus expectations for earnings have risen to $390 per share from $350 per share earlier in the year.5 We assumed a $350 figure in 2027 earnings when we established our 7,700 price target for the S&P 500 at year-end 2026. If $390 in earnings is achieved, 7,700 represents only a 19.5 times multiple, versus the 22 multiple we deem to be realistic; hence, there could be some upside to our year-end target this year.

So…what could go wrong?

What are we watching? There are a couple of items that could cause us to become concerned and cautious. They include:

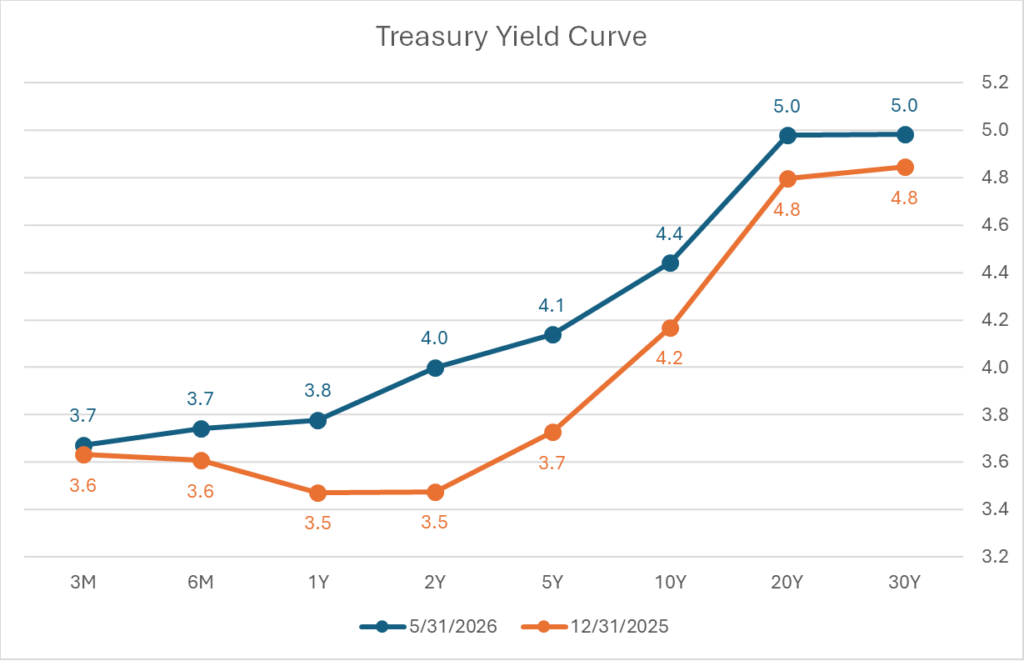

- The future trend in bond yields: Bond yields have not so quietly drifted back up as oil prices have elevated and inflationary pressures have risen. The two-year Treasury has risen post-war and is now yielding more than the current Fed Funds rate. That may signal bond investors think the Fed should consider a modest rate hike, rather than a cut, as its next move given the resilient economy, stable labor market trends and war-related supply constraints that are driving prices higher.

Similarly, the 10-year Treasury is yielding roughly 4.5% at present. This is actually spot on the rate we forecast for the 10-year in our base case assumptions, but it’s up from the 4% level at the beginning of the year. The 30-year is now yielding over 5%, a sustained level we haven’t seen since 2007. We don’t think these higher levels and the pace in the rate of change is worrisome at present, but should this accelerate, this could be a headwind or governor on further stock market gains. To envision rates being a greater issue for the economy and markets, we would need to see a sharper rise in rates from here coupled with an extension in credit spreads. Should this occur, we would become much more cautious.

- Fed policy in transition: Speculation about impacts of Fed policy and leadership transition continues, but they’re on top of it! The Fed has done an impressive job threading the needle regarding balancing the risks of rising inflationary pressures and potential slowdown in employment and economic growth.

So far, we think they get a grade of A on this dual mandate. However, the coming leadership transition adds a new layer of uncertainty for markets. Up to this point, the Federal Reserve has largely succeeded in maintaining its independence and staying data dependent, working to bring inflation under control without choking off the economy. That has been no small feat.

Even with inflationary pressure tied to higher energy and commodity prices, the Fed’s approach has remained measured and appropriately cautious. In our view, the current wait-and-see, data-dependent approach remains the right one.

What adds some uncertainty now is the transition to Kevin Warsh as Chair. That new variable understandably has investors a bit wary and watchful. Still, it’s important to remember that the Chair is not a supreme leader—the Fed is a committee, and effective leadership requires building consensus rather than battling against it. Mr. Warsh is very qualified to be Chair, and our expectation is that he will not prove overly disruptive, but this is clearly something both we and the markets will be monitoring closely in the months ahead.

Wrap-up

In conclusion, we remain positive at a high level and maintain our expectations for double-digit equity returns in 2026. That said, we don’t expect a straight line to new highs. We still envision plenty of volatility and bumps along the way.

Catalysts for these air pockets? For starters, the war in Iran is not resolved and further delays in reopening the shipping lanes obviously could cause periodic mood swings. Similarly, the build-up to the mid-term elections later in the fall might impact psychology from time to time. Messaging from new leadership at the Fed may become opaque compared to the communication philosophies employed by Jerome Powell when he was Fed Chair, and this may annoy investors at times. These issues could inspire temporary shifts in sentiment.

More concerning, we must acknowledge that there are some fundamental cross currents stirring within the still positively trending fundamental data. Earnings growth is robust, but it may soon be in a battle to outcompete the risks of rising interest rates and inflationary pressures. Earnings growth is likely to win out over these forces, but if rates rise enough and credit spreads stretch out enough, that could spark a more permanent pullback in the market.

Source: FactSet

Source: Data sourced from FactSet as of 5/21/2026.

In terms of future stock market leadership, we foresee the number of and variety in winning companies continuing to broaden out in second half of 2026. However, the magnitude and speed of the gains in stock prices in certain sectors and industry groups—e.g. semi’s—is head spinning and has caught our attention.

While these price moves appear justified by the revenue and earnings growth these companies are posting, future headlines about a potential backup in interest rates or cutbacks in capital spending budgets could spark more significant pullbacks in certain high-flying groups.

We might see a series of rotational shifts and corrections in certain areas of the market while the overall market continues to advance. This makes concentrated positioning all the more dangerous and our thesis of RAD and active stock selection increasingly relevant. Stay tuned!

Sources:

1. Source: FactSet. All index returns were sourced from FactSet on 5/29/26

2. Source: Bureau of Labor Statistics; https://www.bls.gov/ces/

3. Source: Multiple sources can confirm this data here is one from the Wall Street Journal; https://www.wsj.com/livecoverage/stock-market-today-dow-sp-500-nasdaq-05-26-2026/card/one-thing-i-m-watching-the-great-ai-buildout-hczrva3jdaiaUKmFBqAW

4. Source: FactSet

5. Source: FactSet. Estimates are the FactSet consensus.

This commentary is provided for informational and educational purposes only. As such, the information contained herein is not intended and should not be construed as individualized advice or recommendation of any kind.

The opinions and forward-looking statements expressed herein are not guarantees of any future performance and actual results or developments may differ materially from those projected. The information provided herein is believed to be reliable, but we do not guarantee accuracy, timeliness, or completeness. It is provided “as is” without any express or implied warranties.

Equity securities are subject to price fluctuation and investments made in small and mid-cap companies generally involve a higher degree of risk and volatility than investments in large-cap companies. International securities are generally subject to increased risks, including currency fluctuations and social, economic, and political uncertainties, which could increase volatility. These risks are magnified in emerging markets.

Fixed-income securities are subject to loss of principal during periods of rising interest rates and are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors before investing. Interest rates and bond prices tend to move in opposite directions. When interest rates fall, bond prices typically rise, and conversely, when interest rates rise, bond prices typically fall.

There is no assurance that any investment, plan, or strategy will be successful. Investing involves risk, including the possible loss of principal. Past performance does not guarantee future results, and nothing herein should be interpreted as an indication of future performance. Please consult your financial professional before making any investment or financial decisions.

Indexes referenced are unmanaged and cannot be directly invested in. For index definitions visit https://www.marinerwealthadvisors.com/index-definitions/.

Mag 7 stocks refer to Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla.

Mariner is the marketing name for the financial services businesses of Mariner Wealth Advisors, LLC and its subsidiaries. Investment advisory services are provided through the brands Mariner Wealth, Mariner Independent, Mariner Institutional, Mariner Ultra, and Mariner Workplace, each of which is a business name of the registered investment advisory entities of Mariner. For additional information about each of the registered investment advisory entities of Mariner, including fees and services, please contact Mariner or refer to each entity’s Form ADV Part 2A, which is available on the Investment Adviser Public Disclosure website. Registration of an investment adviser does not imply a certain level of skill or training.