2%+ growth in 2026

Read time: 9 minutes

“We’ve thrown absolutely everything at it, including a government shutdown, and yet it doesn’t skip a beat.” – Mohamed El-Erian, Allianz chief economic advisor

The comment above was made by Mohamed El-Erian, the esteemed chief economic advisor from European financial services giant Allianz, in a recent interview regarding the U.S. economy. El-Erian served as president and co-chief investment officer at PIMCO, one of the nation’s largest active bond management firms (talk about someone smarter than me).

For all of 2025, we’ve been calling for GDP growth of 1.5% to 2.0% this year. After Real GDP growth of -0.6% in the first quarter1, we’ve witnessed an acceleration in growth as the year has unfolded. If the third and fourth quarter GDP growth comes in around where I anticipate, we should see GDP growth of about 2% for all of 2025.

This is a slower growth rate than we have seen, on balance, over the last few years, but I believe many of the trends that have led to the growth acceleration this year are durable as we come into 2026.

One dominant factor in this year’s economic acceleration is the development and eventual buildout of AI (artificial intelligence) capabilities. Some suggest that AI will prove to be as important a development as the moving assembly line and the mechanization of farming—a trend that ultimately helped drive the industrialization of our nation’s economy. While that thought may carry a bit of hyperbole, it’s perhaps the right spirit in which to think of AI.

True, financial risks of failure are rising within the development of AI. McKinsey estimated a whopping $7 trillion of capital expenditures by 2030 to support the AI buildout2. And, if expectations within the labor productivity arena aren’t met, the downside in asset values and in economic well-being may prove significant.

Is a “bubble” being created? Probably.

But so far, so good. Microsoft, Nvidia and other companies that are directly involved in the AI buildout are mostly generating massively positive cash flow and corporate earnings. Is a financial “bubble” being built? It’s hard to say that it isn’t. But there are rational and irrational bubbles.

El-Erian said recently, “AI is a rational bubble. It makes sense to overinvest in it, to overspend on it, because the payoff is enormous. But be wary of companies that simply put an AI label on what they do and suddenly attract investment that’s going to end up in tears.”

The payoff in AI development may well be in the same vein as the payoff that came with the industrialization revolution: an increase in labor productivity that led to a significant upward push in social wealth. That development shaped and changed the workforce in our country for the following century.

The focus of both revolutions was and is centered on sustainable worker productivity gains.

A history lesson

Let’s take a trip through history: During the Civil War, a majority of the nation’s workers were farmers. Farming was primarily a labor-intensive business, as the mechanization of food production hadn’t yet been developed. To feed itself, the nation needed to have the majority of its workers in the farming business. The ability of the economy to create sustainable, societal wealth through excess production was limited, as the country was literally living hand-to-mouth.

The mechanization of the farming business brought forward a massive increase in agricultural productivity. This allowed many workers to leave the farm and move to the cities to work in factories, making more income and living safer lives. The ability of the economy to create more than it consumed was enhanced, as was societal wealth creation.

According to U.S. Census data, roughly 50% to 55% of the nation’s workers lived on farms in 1860. By 1930, roughly 24% of the workforce lived on farms, as a majority of the nation’s workforce had moved from the farms to cities. Today, less than 3% of workers farm for a living3.

That was a labor revolution. While I’m not sure that today’s AI revolution will eventually have a similar impact, the upcoming change could be major.

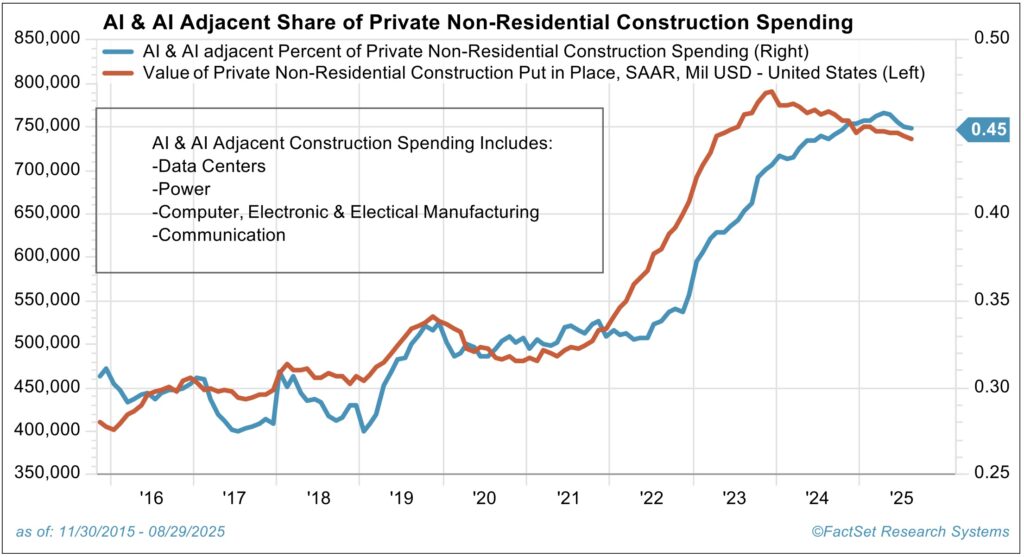

Source: FactSet

There will be winners and losers in AI development. Some speculate that AI development is a revolution as to how people will work. The chart above shows that roughly 45% of all nonresidential construction spending is now tied to AI and AI-adjacent buildout—including spending on data center, power and computer/communication manufacturing—up from 30% a mere 5 years ago.

Not only is the absolute level of spending increasing, but a greater proportion is being dedicated to the buildout of AI; serious capital is being deployed to finance the AI effort.

The importance of worker productivity

Let me throw some numbers at you: one method of calculating GDP growth is counting the number of workers in the economy and then calculating the productivity of those workers. This is called the “output” method by economists. The other two methods are the “expenditure” and the “income” methods. We’ll focus on the output method today.

The output computation method counts the growth in the number of workers in the economy and calculates the productivity rate of those workers. So, we only have two variables to consider. Let’s take a historical view of real GDP growth, labor force growth and resulting labor productivity growth:

| Period | Annual GDP growth | Labor force | Productivity |

| 1950 – 1990 | +3.6% | +1.8% | +1.8% |

| 1990 – 2010 | +2.6% | +1.2% | +1.4% |

| 2010 – 2024 | +2.4% | +0.7% | +1.7% |

(Source: St. Louis Federal Reserve)

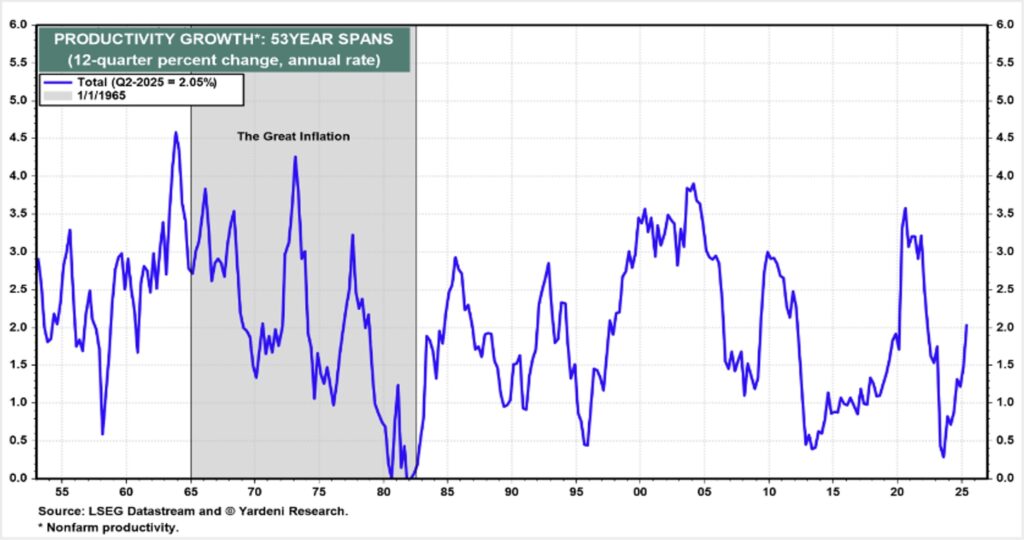

Over long enough periods, worker productivity growth has remained steady. While this hasn’t been the case annually (as noted in the chart below that shows rolling 3-year productivity growth rate), the rate has been consistent over different multi-decade periods. What hasn’t been consistent has been growth in the labor force; more recent growth in the labor force has been only 39% as robust as was the case from 1950 to 1990. The aging of the population and the lowering of the birth rate has led to slower labor force growth rates.

Source: LSEG Datastream and Yardeni Research

There is an old saying in economic forecasting: Today’s demographics are tomorrow’s reality.

Labor force growth is driven by historical birth rates and immigration. The decrease in the U.S. birth rate from 24 births per 1,000 people in 1950 to today’s 12 births per 1,000 people suggests the future growth in the labor force will be more dependent on immigration than in the past. How immigration evolves from here will play an important role in shaping that outcome.

Finally, the U.S. Census Bureau suggests population growth in the U.S. will average +0.4% between 2025 and 2035. Compare that to U.S. population growth of +1.3% per year from 1950 to 1990.

So, the future longer-term economic growth rate will rely more heavily on worker productivity growth than in the past. The good news is AI promises to provide the means for labor productivity growth to accelerate back toward a sustained 2% economic growth rate.

I’m calling for 2026’s economic growth rate to come in above 2%, and perhaps substantially above 2%. I’m suggesting a probability weight of 70% of this outcome is currently appropriate.

Some risks present

Over the shorter term, there are, of course, risks to this optimistic economic outlook—many of which have the capability of throwing our economic outlook into a cocked hat. A few of the risks are as follows:

- China and Taiwan: Will China blockade Taiwan?

- Data center overbuild: “Circular” overbuilds are occurring; will this lead to an unwinding of the AI story? If so, Main Street along with Wall Street will suffer.

- “Levered” risk taking in equities: One-quarter of new ETFs this year have been single stock, or multi-stock levered offerings. Risk-taking levels on Wall Street may be troublesome.

- Dollar drop: The dollar is down this year to foreign currencies. What happens if the dollar drops further? Will the Federal Reserve decide they need to support the value of the dollar by raising interest rates, something most aren’t considering?

- Private credit implosion: As an asset class, Moody’s estimates that private credit will reach over $3 trillion in value by 2028. Retail investors are now coming into the class, possibly indicating a maturing credit trend.

- Independence of the Fed from political persuasion: It’s important for the Fed to retain its independence from political pressure. If that independence is questioned by global investors, the dollar and the Treasury market may pay the price.

- Political polarization: I won’t go into this issue in depth, but it’s clear that many Americans in the broad middle of the political spectrum are starting to feel increasingly caught between the extremes. Remember one of my life’s truisms: “All of life is a careful seeking of balance.”

I don’t expect to see these risks come to pass, but if one or more happens to occur, the 2%+ growth I’m looking for may be thrown off course.

A final word

While our country faces challenges, the people in other parts of the world also have their economic plate full of issues. Regarding the worker productivity issue, while the U.S. will need to propel productivity growth higher in the years ahead, we’re at least starting near the front of the global pack on this issue.

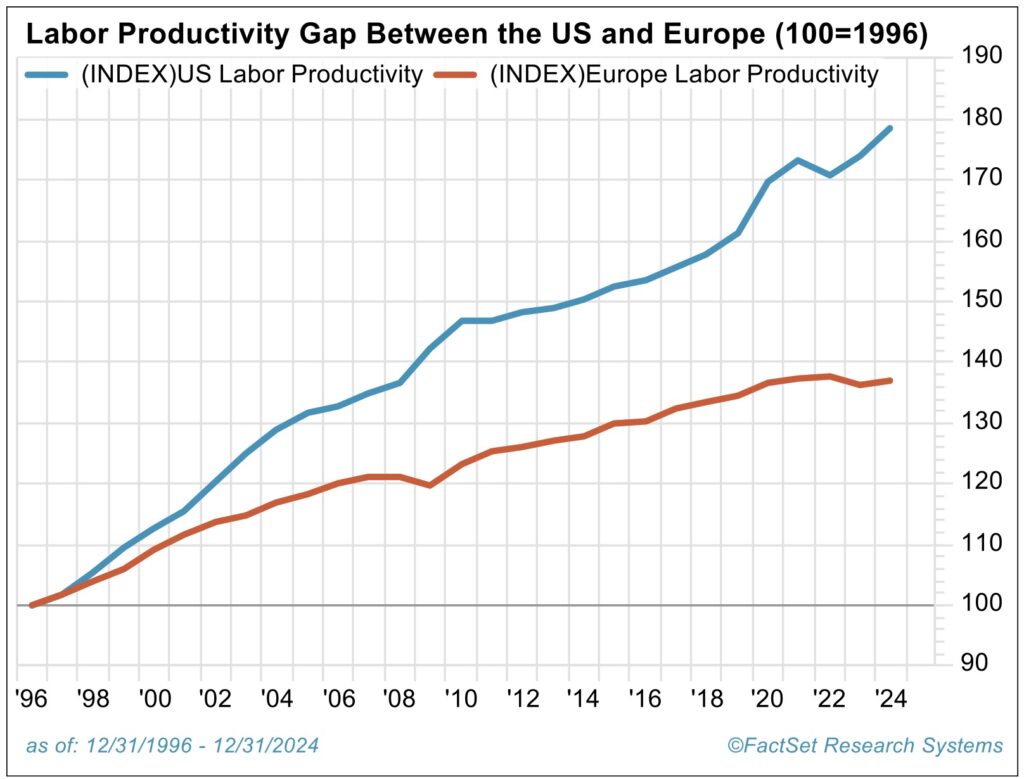

Source: FactSet

Above find a chart of worker productivity growth trend differences between the U.S. and Europe, from 1996 to present. Not only has European population growth been lower than the U.S., but their worker productivity growth rates have also been lower. Socialism may not work as well economically as some expect, or hope.

Thank goodness we all live in the U.S. While we have our challenges and problems, from an economic perspective, the U.S. is still the “King of the Hill.”

Sources:

1Bureau of Economic Analysis

2McKinsey and Company; https://www.mckinsey.com/industries/technology-media-and-telecommunications/our-insights/the-cost-of-compute-a-7-trillion-dollar-race-to-scale-data-centers

3US Census Bureau and US Department of Agriculture

This commentary is provided for informational and educational purposes only. As such, the information contained herein is not intended and should not be construed as individualized advice or recommendation of any kind.

The opinions and forward-looking statements expressed herein are not guarantees of any future performance and actual results or developments may differ materially from those projected. The information provided herein is believed to be reliable, but we do not guarantee accuracy, timeliness, or completeness. It is provided “as is” without any express or implied warranties.

There is no assurance that any investment, plan, or strategy will be successful. Investing involves risk, including the possible loss of principal. Past performance does not guarantee future results, and nothing herein should be interpreted as an indication of future performance. Please consult your financial professional before making any investment or financial decisions.

Mariner is the marketing name for the financial services businesses of Mariner Wealth Advisors, LLC and its subsidiaries.

Mariner is the marketing name for the financial services businesses of Mariner Wealth Advisors, LLC and its subsidiaries. Investment advisory services are provided through the brands Mariner Wealth, Mariner Independent, Mariner Institutional, Mariner Ultra, and Mariner Workplace, each of which is a business name of the registered investment advisory entities of Mariner. For additional information about each of the registered investment advisory entities of Mariner, including fees and services, please contact Mariner or refer to each entity’s Form ADV Part 2A, which is available on the Investment Adviser Public Disclosure website. Registration of an investment adviser does not imply a certain level of skill or training.