Ramifications of Iran war

Read time: 9 minutes

The quest to keep nuclear weapons out of the hands of Iranian leaders has been a concern of the U.S. for some time, not just a Donald Trump quest.

I am not a political analyst, so I’m not making a stand on the legitimacy of the U.S. recent actions. But if Iran were indeed on the cusp of possessing nuclear weapon capability, our nation’s leaders have long stated that condition (Iran possessing nuclear weapons) could not stand.

Back to something I focus upon: The economic impact of the hostilities.

We all hope the conflict in Iran is winding down. The impact which the capital markets and world’s economy have experienced since the start of the war are significant. Is the war coming to an end, or is the current “stand down” merely a halftime show with more hostilities yet to come? Of course, I don’t know the answer to that question. But away from the war, I am sensing we could be experiencing “peak” inflation, to be followed by a slow unwinding of pricing pressure. I certainly hope this is the case, but PPI (producer prices) have recently been running “hot,” suggesting further inflation pressures are in front of us. If hostilities in the Mideast are over, I stand by my view that global inflation pressures may indeed be peaking. If hostilities resume, oil prices could once again rise, which may bring higher inflation pressure to the world.

Whether the war ends soon or not, I think we have seen enough evidence to draw some conclusions as to the probable economic impact from the war. Recently, Barron’s magazine ran a detailed article1 outlining views of global changes we may witness due specifically to the war. These ramifications, if accurate, will take time to unfold on a global macro scale. The disrupting issues outlined in the article (along with some of my own) are noted below.

- The war disrupted the energy industry, leading to a reshuffling of partnerships and alliances in OPEC with the rest of the Mideast. UAE left OPEC, leaving the Saudis as the main controlling producer of excess oil output. The stability of OPEC’s operating rules has changed.

- How countries think of their own security has changed. Iran physically attacked Kuwait, Qatar, Saudi Arabia and the UAE. Will these countries eventually become closer to Israel, the U.S. or both? Until the war, this type of partnership was unthinkable.

- Oil exporting countries are exploring various new physical distribution channels away from the Strait of Hormuz. Along with oil, the delivery of other raw materials beyond oil was negatively affected by the Strait’s closure. Shipments of helium, fertilizer, sulfur and aluminum were all delayed or eliminated for a period.

- Egypt, Turkey, Jordan, Iraq and Syria are trying to position themselves as alternative transit hubs to bypass the Strait. This is leading to talks about major infrastructure expenditures by exporting counties and those who would benefit from the increased spending on additional pipelines, and overall transport infrastructure.

- Commodity importing countries are looking to expand relations with non-Mideast commodity producing countries to be used as alternative supply channels. From Japan to Europe, all are looking for new oil import partners.

- Increasing alternative (renewable) energy production has taken on additional importance for many countries. This is particularly true in Europe. Expect to see additional spending to electrify energy use in many parts of the developed world. In a recent poll taken by the E3G group of 2000 business leaders in 18 countries, 91% of those polled think electrification improves energy security. Additionally, 79% of those polled believe geopolitical instability has made their own business shift to consider supporting electric energy generation.2

- Along with renewables, nuclear energy generation will likely become a bigger piece of the energy creation puzzle.

- The day of just-in-time inventory saturation may be behind us. This may be truer for commodity-based consumption needs.

- With the de-emphasis by the U.S. of NATO’s importance, many countries are exploring and expanding defense expenditures. Globally, national security has taken center stage in developed nations’ planning.

This is a big bag of newly found (or intensified) security and economic concerns the war has brought forward. I’m sure there are other issues with which the world’s leaders are wrestling, but the nine items above are good starters for consideration. Let’s expand on the commodity importation needs.

Oil imports and reserve replacement

Wars always have lasting effects on both political and economic outcomes. From an economic standpoint, I believe we will see long-lasting changes occurring due to the war events.

The world understands that it needs oil on a continuous basis. Many nations will likely increase their official oil reserve levels. Below find oil reserve levels prior to the start of the Iran conflict and daily consumption levels.

| Oil Reserve (bbl.) | Daily Consumption (bbl.) | Day’s Supply | |

| China | 1.4 billion | 16.4 million | 86 |

| U.S. | 415 million | 20.4 million | 21 |

| Japan | 260 million | 3.1 million | 83 |

| Germany | 177 million | 2.0 million | 88 |

| France | 120 million | 1.5 million | 80 |

| Italy | 76 million | 1.2 million | 63 |

| U.K. | 68 million | 1.4 million | 48 |

| S. Korea | 190 million | 2.5 million | 76 |

| Taiwan | 131 million | 0.9 million | 143 |

Source: Compiled from International Energy Agency, U.S. Energy Information Administration, and national strategic petroleum reserve data; reserves and consumption are approximate.

The IEA (International Energy Agency) has set a recommended reserve of 90 day’s consumption as the “standard” for the supply a country needs to carry. That recommendation was made prior to the Iran conflict. I suspect that suggested level will rise as we move forward, due specifically to the supply disruption provided by the Iranian war. Digging into the IEA’s website shows that the agency hasn’t yet made a statement regarding new, higher recommended oil reserve levels. Perhaps they are waiting to see how and when the Iranian war is resolved.

When the IEA releases their new thoughts concerning oil reserves, the replacement in expended oil reserves along with new, higher recommended levels should keep oil prices from falling back into the $60 per bbl. level we saw prior to the breakout of Iranian hostilities for some period.

From the supply standpoint, the Mideast is anything but stable. How may countries which import not only oil, but other important industrial raw materials act going forward? Perhaps sometime in the future the same type of import freeze we have recently seen in the Mideast may occur with other “strategic” commodities such as fertilizer, aluminum, copper, iron ore and nickel.

Therein lies the logic behind the establishment and nurturing of multi-supply channels for all strategic industrial metals along with oil.

Commodity supply roadmap: Expanding the discussion

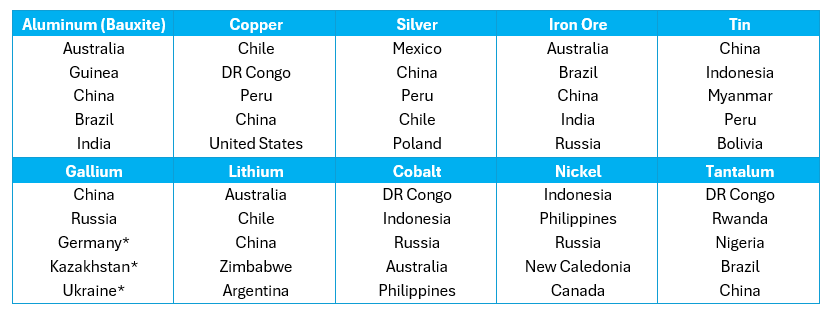

Access to 10 key industrial metals is essential for countries that manufacture technology products, though demand varies by industry and product type. The list below highlights these metals and the top five producing countries for each.

*Gallium is somewhat unique because the USGS reports production differently than traditional mine output, since gallium is recovered as a byproduct of bauxite and zinc processing. The top producers can vary depending on whether the source measures primary production, refined gallium, or capacity.

Source: U.S. Geological Survey, Mineral Commodity Summaries 2026 (February 2026).

A simple way of thinking about which parts of the world have been blessed with large endowments of critical industrial and technology metals is to look at where the leading producing countries are located. Across the 50 country occurrences listed in the table, 14 are in the Asia-Pacific region (excluding China), 11 are in South America, 7 are in Africa, and China alone accounts for 8 occurrences. Europe accounts for 7, while North America accounts for just 3.

Although the United States and Canada are major energy producers, North America is comparatively less represented among the world’s leading producers of many industrial and technology metals. As a result, the U.S. remains dependent on imports for a number of critical minerals that support modern manufacturing and advanced technologies—and this discussion doesn’t even include rare earth elements, which present another important strategic consideration.

All eyes are currently on the availability of oil due to the Iran war. The lessons learned from the Strait of Hormuz closure can be applied to the import of other, strategically important commodities. We in the U.S. are able to supply the bulk of our own oil needs and are able to feed ourselves. But we need to maintain good working relations with countries around the world as we don’t mine nearly all our needs for commodity metals.

Capital market takeaway

So, what does this input mean for investors in the capital markets? First, the U.S. isn’t an island nation in itself. Our economy is highly tied to the import of various raw materials. Of the noted 10 strategic metals noted, the U.S. is a top world producer in only one of those. We need to maintain good relations with a number of countries in various parts of the world for our economy to function well.

Secondly, of the noted countries which mine the 10 strategic metals, 24 are “emerging” economies in Africa, South America or the Pacific regions (this count doesn’t include China which is noted in 8 entries). The production of strategic metals is an emerging economy game.

In my view, all investors should take this fact into consideration when thinking of the allocation of capital. While many of the countries noted aren’t the most politically stable countries in the world, they all have something to share with us, something we and the rest of the world need. So, when investors question placing capital to work outside of the U.S., perhaps this work will outline a number of reasons.

Sources:

1. Sabrina Escobar, “4 Ways the Iran War Already Changed the Global Economy,” Barron’s, June 18, 2026. https://www.barrons.com/articles/iran-war-reshaped-global-economy-commodity-security-oil-alternative-energy-db12ddf7

2. Source: E3G, https://www.e3g.org/news/new-business-polling-electrification-support

This commentary is provided for informational and educational purposes only. The information contained herein is not intended and should not be construed as individualized investment advice or a recommendation regarding any particular investment, strategy or course of action.

The opinions and forward-looking statements expressed herein are those of the author as of the date of publication, are subject to change without notice, and are not guarantees of future events or future investment performance. Actual results or developments may differ materially from those discussed.

The information provided herein is derived from sources believed to be reliable; however, we do not represent or warrant its accuracy, completeness or timeliness. It is provided “as is” without express or implied warranties.

There is no assurance that any investment, plan or strategy will be successful. Investing involves risk, including the possible loss of principal. Past performance is not a guarantee of future results, and nothing contained herein should be construed as an indication of future performance. Investors should consult with their financial, tax and legal advisers before making investment or financial decisions.

Mariner is the marketing name for the financial services businesses of Mariner Wealth Advisors, LLC and its subsidiaries. Investment advisory services are provided through the brands Mariner Wealth, Mariner Independent, Mariner Institutional, Mariner Ultra, and Mariner Workplace, each of which is a business name of the registered investment advisory entities of Mariner. For additional information about each of the registered investment advisory entities of Mariner, including fees and services, please contact Mariner or refer to each entity’s Form ADV Part 2A, which is available on the Investment Adviser Public Disclosure website. Registration of an investment adviser does not imply a certain level of skill or training.