Economic Outlook September 2025: He Blinked

Read time: 9 minutes

Well, he blinked. What am I referring to? At his recent speech in the Jackson Hole central bank confab, Jerome Powell indicated that people should anticipate the Federal Reserve (the Fed) will lower the Fed Funds rate at their September meeting.

The administration has been pressuring the Fed to make this decision for some time, and Powell and his team have resisted until now. As of Sept. 2, 2025, the financial futures market is placing a 92% probability that the Fed will reduce rates following their meeting in September.1

Why the change? The likely aim is to push up GDP growth rates, as many indictors are suggesting the U.S. economy’s growth rate has slowed. In his comments from the Jackson Hole confab, Chairman Powell stated that “The balance of risks appears to be shifting.”

“It is a curious kind of balance that results from a marked slowing in both the supply of and demand for workers,” said Powell.2

He went on to say that the “unusual situation” is supporting higher risks of worse than expected labor market outcomes (higher unemployment and slower job creation).

We’ve been expecting the jobs market to slow, along with a deceleration in GDP growth compared to 2024. Powell’s shifting stance remains part of our “3 Yards and a Cloud of Dust” core economic theme for 2025.

Given where the three central banks (Atlanta, New York and Dallas)—which monitor and model expected quarterly GDP growth rates on a daily basis—have positioned their estimates, third quarter GDP growth is currently expected to be in the 2.6% range,3 down from the second quarter announced GDP growth rate of 3.3%.4

GDP growth this year has been running at an annualized rate of 1.8%, in-line with our “3-Yards” forecast of 1.5% to 2.0% growth for the year—assuming growth comes in at 2.6% in the third quarter.

Consumer – Spending and Job Creation Weakening

Where do we see growth weakening—but not yet “weak”? Chairman Powell is justified in thinking that the risks in the economy have shifted from probable inflation issues towards a weakening growth profile. After all, “real” consumer spending (personal consumption expenditures trailing three months, annualized) has slowed from a long-term average of 2.4% to 1.0% year-to-date to -0.4% over the last two months.5

Nonfarm payroll growth has slowed in-line with consumption growth. In the latest jobs report, the Bureau of Labor Statistics (BLS) reports that a mere 73,000 jobs were created during the month of July, and an even weaker level of 35,000 jobs had been created during the last three months, on average. These numbers can be compared to longer-term monthly job creation levels of 158,000 (2010 – 2025).6

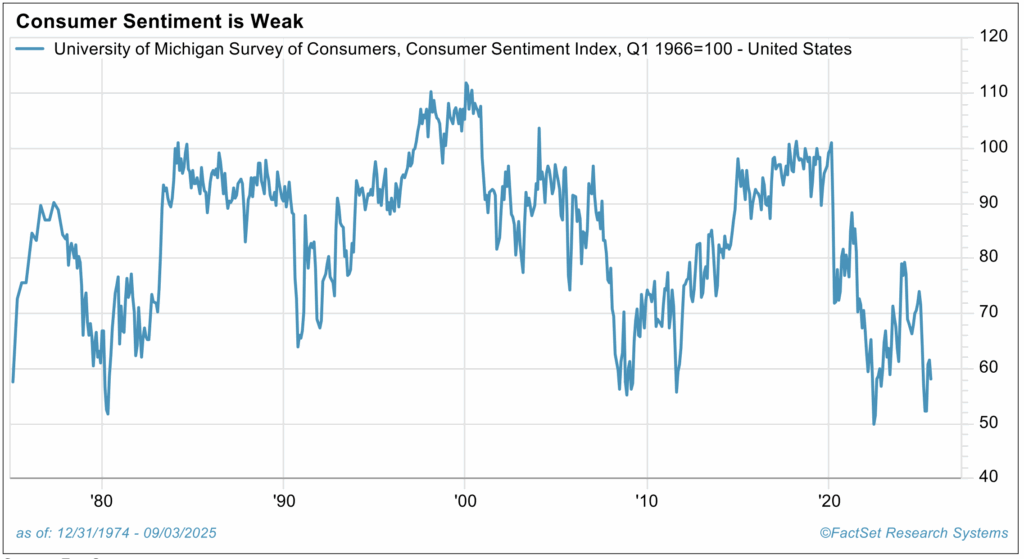

Source: FactSet

The weaking consumer economic profile is evident in the latest University of Michigan’s Consumer Sentiment Index (chart above), which now stands at 58.2—down from 74 at the start of 2025 and well below a longer-term average of 84.3 (1975-2025).

I view sentiment data as a measure of people’s willingness to consume and not the ability to do so, which is driven by job availability readings.

By many measures, consumer confidence in economic growth has weakened since the start of the year. Again, these developments are in-line with our main economic theme for this year: “3 Yards and a Cloud of Dust.”

With this show of economic sluggishness, Chairman Powell “blinked” at his Jackson Hole presentation and suggested that recent economic weakness may be pushing the Fed to consider re-igniting their interest-rate reduction program.

Inflation Update

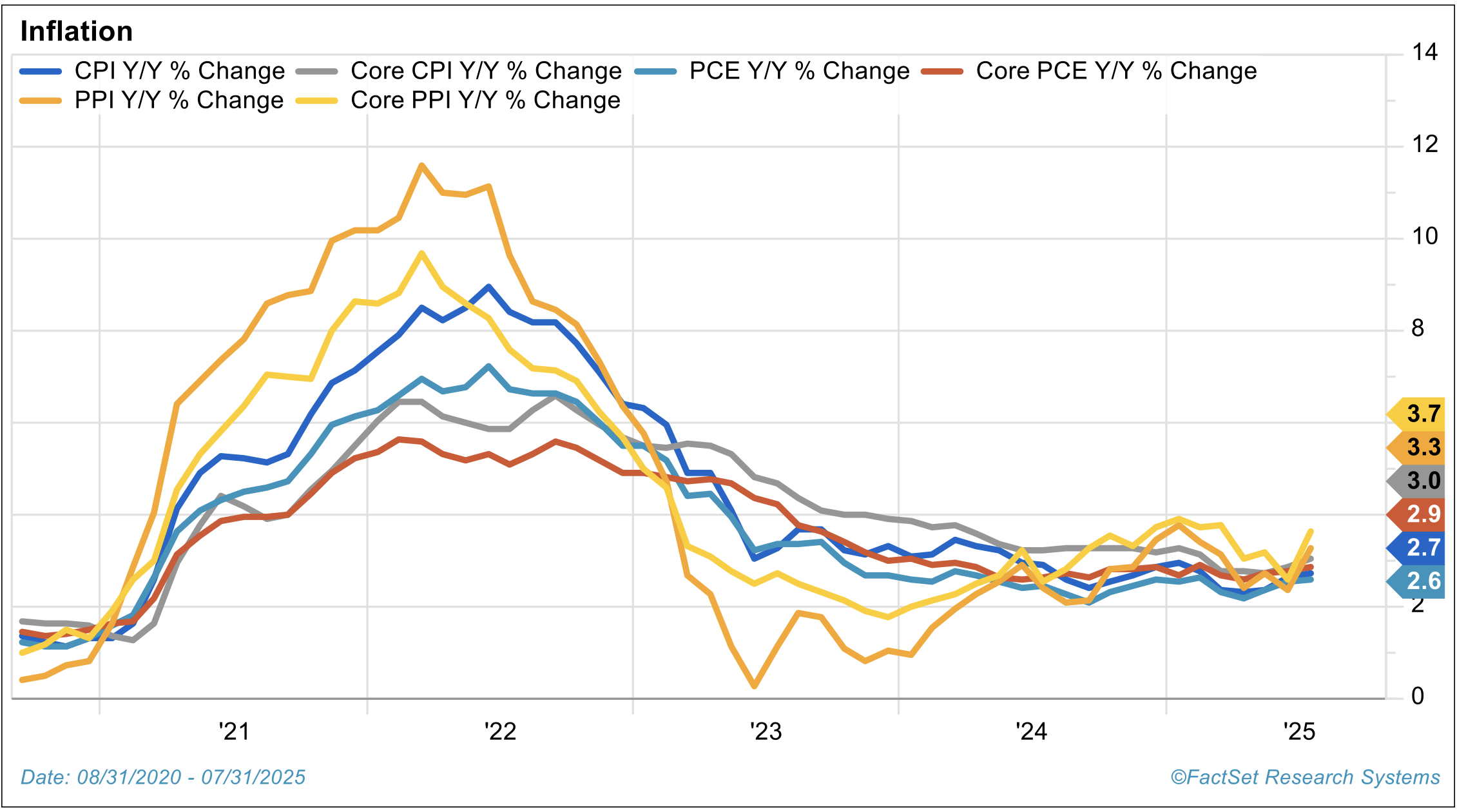

Source: FactSet

I’ve been maintaining the view that the shorter-term economic impact of Trump’s “4 Buckets” (tax package, tariff activity, undocumented immigrant deportations and DOGE program) carries real risk of putting upward pressure on inflation. Trump’s administration states that we aren’t seeing any real inflationary push.

I, on the other hand, see the headlights of rising inflationary pressure down the road, and believe higher inflation pressures may be heading in our direction. Both tariffs (higher retail prices for various goods) and the deportation of undocumented aliens (labor cost pressures) contain the “stuff” which could push inflation upward.

Yet the President’s administration is telling us that inflation continues to weaken. Are they right? Well, kind of. Data pertaining to consumer and producer price increases are as follows.7

| July 2025 | March 2025 | One Year Ago | |

|---|---|---|---|

| Consumer Price Index | 2.7% | 2.4% | 2.9% |

| Core PCE Price Index | 2.9% | 2.7% | 2.7% |

| Producer Price Index | 3.3% | 3.2% | 2.4% |

The 12-month trailing CPI now stands at 2.7%, up from 2.4% in March of this year, but down slightly over the last year. The “core” PCE is now at 2.9%, flat over the last few months.

The administration’s statement that inflation has declined is marginally correct, but inflation isn’t declining significantly and isn’t near the Fed’s 2% “target” rate. With tariff rates starting to impact pricing, I don’t expect we’ll see a 2.0% print on trailing inflation—the Fed’s stated inflation “target”—until the next recession.

Take note of the Producer Price Index (PPI) data on the chart and table above; tariff payments have been initiated recently and are starting to be reflected in the PPI data. The PPI was around 0% annualized about 18 months ago and is now 3.3%. Let’s explain how tariff payments work.

Inside Baseball: Tariffs—Who Pays?

Tariffs aren’t actually paid by the companies or countries which export goods into the U.S. Instead, the importer of the good pays the tariff directly to the U.S. Treasury.

For example, if Walmart orders goods from a Chinese manufacturer, Walmart pays the tariff tax on the goods, and not the Chinese company. Now, Walmart has the option to either pass the tax on to a U.S. customer, “eat” the tax in their profit margin or squeeze the Chinese company to pay a portion or all of the tariff tax. Two of these three possibilities hurt U.S. entities and not the foreign exporting company.

The following excerpt (Feb. 15, 2025) regarding tariffs is from the well-regarded Tax Foundation and gives us a deeper understanding of how tariffs work:

When the US imposes tariffs on imports, businesses in the United States directly pay import taxes to the US government on their purchases from abroad. The economic burden of the tariffs, however, could fall on others besides the US business directly paying the tax, including foreign businesses selling goods to US businesses (if foreigners lower their prices to absorb some of the tariffs) or US consumers ultimately purchasing the goods (if US businesses raise their prices to pass on the tariffs).

Historically, economists have found that foreign firms absorbed some of the burden of tariffs by lowering their prices, resulting in a combination of foreign businesses and domestic firms and consumers sharing the burden of tariffs. In contrast to past studies, however, recent studies have found the Trump tariffs were passed almost entirely through to US firms or final consumers.

Economists Pablo Fajgelbaum, Pinelopi Goldberg, Patrick Kennedy, and Amit Khandelwal examined the tariffs on washing machines, solar panels, aluminum, steel, and goods from the European Union and China imposed in 2018 and 2019. They found that US firms and final consumers bore the entire burden of tariffs and estimated a net loss to the US economy of $16 billion annually, including more than $114 billion in losses to firms and consumers, offset by small gains to protected producers and revenue gains to the government.

There’s often a misconception that tariffs don’t harm U.S. interests. In reality, most economists recognize that tariffs are damaging to an economy, as they tend to spawn inflationary pressures. I’ve been suggesting that an average 18% tariff rate applied to imports to the U.S. could increase the CPI by around 0.5% by the end of this year.

Final Word

On an indirect basis, tariffs tend to act as another “tax” on either U.S. businesses or U.S. consumers. I continue to stand behind my view that Core PCE will move upward toward 3.0% by year end (currently 2.8%).

This is likely as low-tariff inventories that built up in the first quarter of this year are worked off and replaced with higher-tariff inventories—increased costs that, in many cases, will be passed on to the consumer.

Chairman Powell’s expected interest rate decrease (which may indeed occur following the Fed’s September meeting) may be the only rate decrease we see this year. This may be particularly true if Core PCE rates start ramping upwards.

Let me finish by stating a couple of economic maxims which I have found to be true and relevant to our tariff discussion: In economics there’s no such thing as a free lunch, and in economics there are no solutions, only tradeoffs. Both maxims are currently at work.

Sources:

1CME FedWatch Tool; https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

2Federal Reserve; https://www.federalreserve.gov/newsevents/speech/powell20250822a.htm

3This is the simple average of the three forecasting tools as of 9/2/2025; https://www.atlantafed.org/cqer/research/gdpnow; https://www.newyorkfed.org/research/policy/nowcast/#nowcast/2025:Q3; https://www.dallasfed.org/research/wei

4Bureau of Economic Analysis; https://www.bea.gov/data/gdp/gross-domestic-product

5Data Sourced from the BEA; https://fred.stlouisfed.org/series/PCEC96#

6Bureau of Labor Statistics; https://www.bls.gov/ces/

7FactSet

This commentary is provided for informational and educational purposes only. As such, the information contained herein is not intended and should not be construed as individualized advice or recommendation of any kind.

The opinions and forward-looking statements expressed herein are not guarantees of any future performance and actual results or developments may differ materially from those projected. The information provided herein is believed to be reliable, but we do not guarantee accuracy, timeliness, or completeness. It is provided “as is” without any express or implied warranties.

There is no assurance that any investment, plan, or strategy will be successful. Investing involves risk, including the possible loss of principal. Past performance does not guarantee future results, and nothing herein should be interpreted as an indication of future performance. Please consult your financial professional before making any investment or financial decisions.

Mariner is the marketing name for the financial services businesses of Mariner Wealth Advisors, LLC and its subsidiaries. Investment advisory services are provided through the brands Mariner Wealth, Mariner Independent, Mariner Institutional, Mariner Ultra, and Mariner Workplace, each of which is a business name of the registered investment advisory entities of Mariner. For additional information about each of the registered investment advisory entities of Mariner, including fees and services, please contact Mariner or refer to each entity’s Form ADV Part 2A, which is available on the Investment Adviser Public Disclosure website. Registration of an investment adviser does not imply a certain level of skill or training.