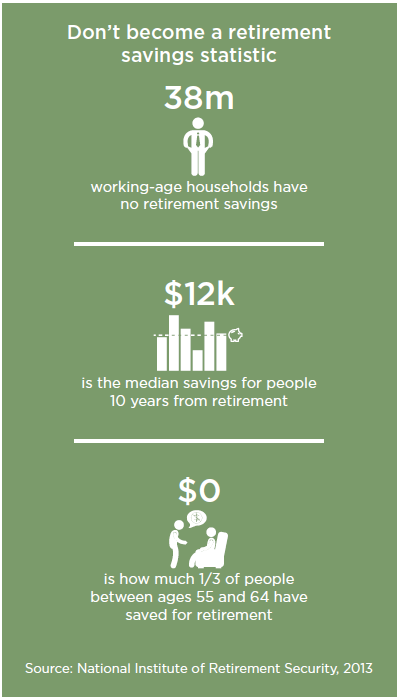

Don’t Rob Your Retirement

Are You Living Within Your Means?

It’s reported that 127.5 million Americans aren’t.* Living beyond your means can be described as: living paycheck to paycheck, no savings for emergencies, no savings for the future.

*Corporation for Enterprise Development, 2012

Working Poor, Living Large

Nearly half of us use all of our paychecks, but spend as if we have more. We purchase things we want while neglecting things we need, like an emergency account or saving enough for retirement.

An important step toward having enough money in retirement is to change your current spending habits.

Save More, Spend Less

It sounds like a simple solution, but is not always easy to implement.

Take stock of your spending habits and make a decision that your future is more important than your present wants. Ultimately, it takes a commitment.

10 Ways To Spend Less

Once you’ve decided to cut back, here are some tips that may help you reduce every day expenses.

BE ENERGY EFFICIENT

Turn out lights, unplug devices not in use, adjust the thermostat, install a few CFL light bulbs and potentially reduce your energy bill by 30%. That equals about $26 a month less than the average $86 a U.S. consumer spends.*

*White Fence Index, November 2013

VISIT THE LIBRARY

Borrow the latest bestseller or DVDs instead of paying $15 to $20 for your own copy.

SHOP AROUND

Get price quotes and see who’s most interested in your business. It also pays to compare costs on bigger ticket items. Save up to 30% on major purchases by comparison shopping.

DON’T SKIP ROUTINE MAINTENANCE

Keep cars and appliances well maintained. It’s cheaper to maintain than to pay for the results of neglect. Plus, items in tip top shape can run more efficiently, saving in fuel and energy costs.

BUY OUT OF SEASON

Christmas decorations in January and swimsuits in September are usually cheaper. You can even buy off-season electronics. For example, the fiscal year of many TV manufacturers begins in April. Look for deals in May on last year’s models.

PRACTICE ORGANIZED SHOPPING

Develop weekly meal plans and make shopping lists before you head to the grocery store. You could save up to $40* a week by not putting frivolous items in your shopping cart.

*100 Ways to Save Money, msnliving.com, 2013

SHOP LESS

The more you shop, the more you buy. People usually buy 54% more when they make quick trips for a few items. Impulse buying accounts for between 50% and 68% of all purchases. Only shop once a week to save.

*Economides, Steve and Annette, America’s Cheapest Family, 2007

USE COUPONS

Coupons can help trim up to 25% off the grocery bill for novice clippers. Veterans have learned to save up to 60%. Also, consider group online offers to save up to 80% for goods, services and entertainment. Buy only what you will use, or what you can stock up on for later.

TAKE YOUR LUNCH

66 percent of workers spend nearly $2,000* a year on eating lunch out. If you brown bag it every day, you could easily cut your lunch costs by about $74 every month.

*Workonomix Survey, Account Principals, 2012

BE ENTERTAINED FOR LESS

Take advantage of free or low-priced events in your community: free concerts, museums and community festivals offer cheap fun. Skip the expensive night out and entertain at home. Dinner and a movie for two can cost well over $100. Enjoy a $3 movie rental and microwave popcorn instead.

This material is provided with permission from American Century. It is for informational purposes only and has been obtained from sources believed to be reliable. While every effort is made to ensure the accuracy of its contents, it should not be relied up on as being tax, legal, or financial advice.

American Century Investment Services, Inc., Distributor © American Century Proprietary Holdings, Inc. All rights reserved.

Mariner is the marketing name for the financial services businesses of Mariner Wealth Advisors, LLC and its subsidiaries. Investment advisory services are provided through the brands Mariner Wealth, Mariner Independent, Mariner Institutional, Mariner Ultra, and Mariner Workplace, each of which is a business name of the registered investment advisory entities of Mariner. For additional information about each of the registered investment advisory entities of Mariner, including fees and services, please contact Mariner or refer to each entity’s Form ADV Part 2A, which is available on the Investment Adviser Public Disclosure website. Registration of an investment adviser does not imply a certain level of skill or training.

Mariner Starts 2026 With $1.8 Billion Dual Acquisition as Advisor Growth Accelerates

2026 retirement plan limits