Social Security: When to Start Receiving Benefits

The nagging question we all begin to ponder as we approach retirement, “When should I begin taking Social Security benefits?” is a complex one that often does not have an easy answer. It depends on your situation and objectives. Here, we provide a general overview of some considerations to keep in mind as you decide when to begin receiving Social Security benefits.

Benefits Eligibility and Age

The earliest an individual can begin receiving Social Security retirement benefits is age 62. The latest an individual can delay receiving benefits is age 70.

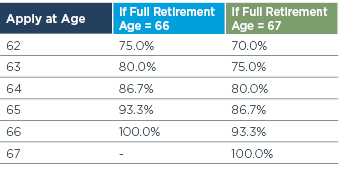

The chart below summarizes the estimated percentages of Social Security benefits an individual would receive based on the age an individual applies for Social Security.

- Full Retirement Age = 66 for people born between 1943-1954

- Full Retirement Age gradually rises to 67 for people born between 1955-1959

- Full Retirement Age = 67 for people born after 1960

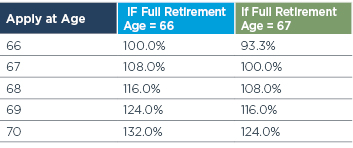

For each year an individual delays claiming benefits past Full Retirement Age, he or she is eligible for an 8 percent increase until the age of 70.

If your goal is to maximize your Social Security benefit during retirement, delaying until age 70 may be a wise choice. The following factors should be taken into consideration when deciding when to claim benefits.

- Health status and life expectancy: If you face significant health problems, it may make sense to claim benefits earlier and avoid waiting until Full Retirement Age. In this case, any benefit, even if it is reduced, may be better than none. If you are in good health and have a long life expectancy, you may decide to delay receiving Social Security benefits until later in order to maximize the amount of your monthly payments.

- Consider your personal situation:When deciding when to claim benefits, consider where your assets are located, and the size of your IRAs. There may be benefits to claim your benefits early. Your wealth advisor can discuss with you what timing makes sense based on your situation.

- Employment status:If you plan on working up to full retirement age and will be earning a high salary over that time horizon, you may consider delaying your benefits. Until you reach full retirement age, Social Security will withhold money from your retirement check if you exceed a certain amount of earned income for the year ($18,240 in 2020).

The Impact of Delaying Benefits

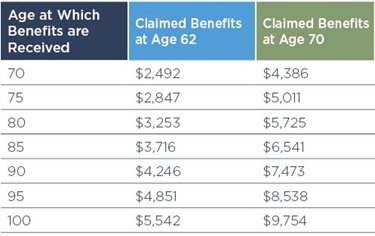

The financial advantage of delaying Social Security can be significant. Your total monthly payments may increase by nearly 60% if you delay benefits from age 62 until 70. The numbers in the table below assume a Primary Insurance Amount (PIA) at age 66 of $2,685 and a 2.7% cost of living adjustment.

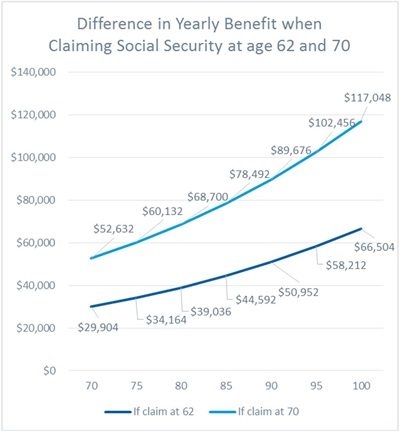

The next graph shows how your yearly benefit may increase when you begin taking payments at age 70 instead of age 62. In this illustration, the yearly payment nearly doubles by age 100 for the individual who delayed receiving benefits.

Spousal Benefits

Spousal benefits allow a spouse to claim either the greater of his/her own Social Security benefit or half of his/her spouse’s full retirement age benefit. (Note: To collect a spousal benefit, your spouse must have already started collecting.) There are many planning strategies when spousal benefits exist; for example, the higher-earning spouse could wait to collect at age 70 to maximize his/ her benefit and then at that point, the other spouse could collect half of the spouse’s full retirement age benefit. And if the lower-earning spouse has their own benefit, they can evaluate starting any time between age 62 and 70. This may provide an opportunity for additional household income.

Conclusion

There is no right answer for when you should begin collecting Social Security. You should take into consideration your anticipated retirement age, health status and financial situation. Your advisor can help create a strategy that best fits your circumstances.

The views expressed are for commentary purposes only and do not take into account any individual personal, financial, or tax considerations. It is not intended to be personal legal or investment advice or a solicitation to buy or sell any security or engage in a particular investment strategy.

Mariner is the marketing name for the financial services businesses of Mariner Wealth Advisors, LLC and its subsidiaries. Investment advisory services are provided through the brands Mariner Wealth, Mariner Independent, Mariner Institutional, Mariner Ultra, and Mariner Workplace, each of which is a business name of the registered investment advisory entities of Mariner. For additional information about each of the registered investment advisory entities of Mariner, including fees and services, please contact Mariner or refer to each entity’s Form ADV Part 2A, which is available on the Investment Adviser Public Disclosure website. Registration of an investment adviser does not imply a certain level of skill or training.